Global Outlook for Wire and Cable

23 April 2026

Chi Lee of CRU outlines the growth drivers, trade pressures and market shifts shaping the sector in 2026 At the IWMA Industry Networking Lunch in February 2026, Chi Lee, Analyst, […]

Chi Lee of CRU outlines the growth drivers, trade pressures and market shifts shaping the sector in 2026

At the IWMA Industry Networking Lunch in February 2026, Chi Lee, Analyst, Wire & Cable at CRU, delivered a clear and timely overview of the forces currently shaping the global wire and cable market. Her presentation balanced optimism with caution. The fundamentals for the sector remain strong, but the trading environment is becoming more complex, with geopolitical tension, tariff intervention, raw material volatility and shifting regional demand all influencing the road ahead.

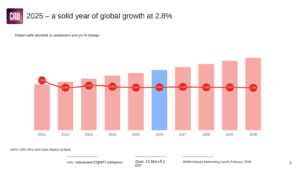

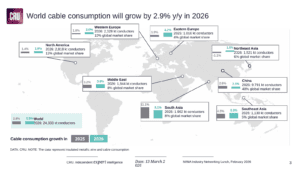

Global cable growth in 2025 was solid at 2.8 percent, and CRU expects global insulated metallic wire and cable consumption to grow by a further 2.9 percent year on year in 2026. That continuing expansion reflects the strength of underlying structural demand across electrification, grid investment, renewable energy, transport transformation and digital infrastructure. Rather than depending on one single end-use sector, the market is now being supported by several major long-term trends at once.

Figure 1: 2025 global growth remains solid at 2.8%

Figure 2: World cable consumption is forecast to grow by 2.9% in 2026

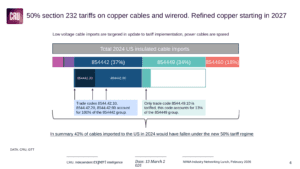

One of the most immediate pressures on the sector, however, is policy. Chi Lee pointed to the impact of updated US Section 232 tariff measures, which now apply 50 percent tariffs on copper cables and wirerod, with refined copper set to follow from 2027. The details matter. Low voltage cable imports are the main area affected, while power cables are largely spared. Even so, the impact is significant, with CRU noting that 43 percent of cables imported into the United States in 2024 would have fallen under the new 50 percent tariff regime.

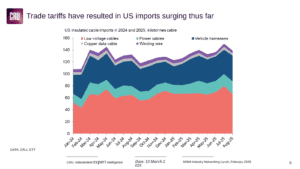

This change has already altered buying behaviour. Imports into the US have surged as customers and distributors move quickly to secure supply before tighter trade conditions take hold. It is a reminder that tariff announcements do not simply affect future pricing, they can reshape short-term trade flows almost immediately.

Figure 3: Updated tariff implementation targets a significant share of US cable imports

Figure 4: US cable imports have surged in response to tariff changes

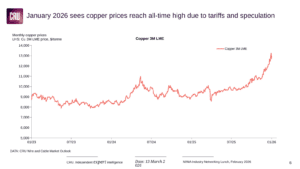

These trade measures are also feeding directly into the raw materials picture. As Chi Lee highlighted, copper prices reached an all-time high in January 2026, driven by a combination of tariff effects and market speculation. For manufacturers, this creates a particularly difficult environment: demand remains healthy, but margins, lead times and customer pricing discussions are all under pressure from metal volatility.

Figure 5: Copper prices hit a record high in January 2026 amid tariff concerns and speculation

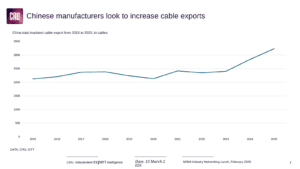

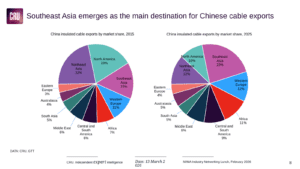

Beyond the United States, the presentation showed how trade patterns continue to evolve elsewhere. Chinese manufacturers are actively seeking to increase cable exports, and Southeast Asia has emerged as the principal destination for that growth. However, it is important to note that Chinese cable exports to Europe remain roughly unchanged compared with a decade ago. This reflects both the strength of regional industrial demand and the broader rebalancing of international trade as supply chains respond to new political and commercial realities. China’s export strategy is therefore not only a story of production scale, but also one of market repositioning.

Figure 6: Chinese manufacturers continue to increase cable exports

Figure 7: Southeast Asia has become the main destination for Chinese cable exports

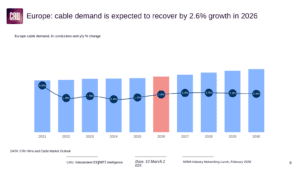

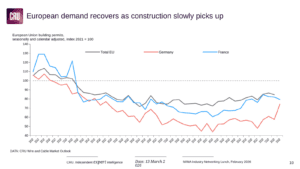

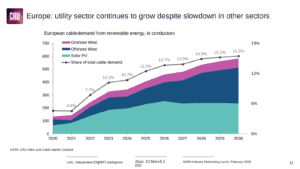

In Europe, the outlook is encouraging, if more measured. CRU expects cable demand in the region to recover by 2.6 percent in 2026, supported in part by a gradual return of construction activity after a weaker period. That recovery is important, but Chi Lee also made clear that Europe’s resilience is not based on construction alone. The utility sector continues to provide a strong foundation for demand, even while other market segments remain softer. Grid modernisation, energy security requirements and long-term transmission investment are all helping to support sustained cable consumption across the region.

Figure 8: European cable demand is forecast to recover by 2.6% in 2026

Figure 9: Construction activity is beginning to support a broader recovery in European demand

Figure 10: Europe’s utility sector continues to grow despite weakness elsewhere

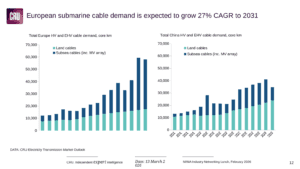

Perhaps the most striking figure in the presentation came from the submarine cable segment. European submarine cable demand is expected to grow at a compound annual rate of 27 percent through to 2031. That level of expansion underlines the scale of investment now being directed towards offshore wind connections, interconnectors and cross-border electricity infrastructure. For many businesses in the wider wire and cable value chain, this remains one of the most technically demanding and commercially attractive growth areas in the market.

Figure 11: European submarine cable demand is expected to grow at 27% CAGR to 2031

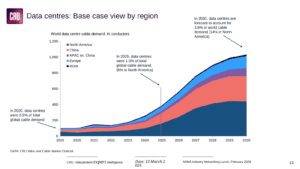

Another major demand driver is digital infrastructure. Data centres featured prominently in Chi Lee’s analysis, reflecting their growing importance as electricity-intensive assets and as a source of specialised cable demand. As artificial intelligence, cloud services and digital connectivity continue to expand, wire and cable demand is increasingly linked not only to the energy transition, but also to the infrastructure underpinning the global digital economy.

Figure 12: Data centre development is creating another strong source of regional cable demand

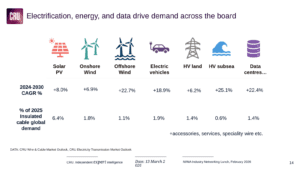

Chi Lee concluded by bringing these themes together under a wider structural picture. Electrification, renewable energy, electric vehicles, high-voltage land and subsea transmission, solar, wind and data centres are all helping to drive market growth across the board. Some of these applications still account for a relatively modest share of total cable demand today, but their growth rates are exceptionally strong and their long-term strategic significance is much greater than their current market size alone might suggest.

Figure 13: Electrification, energy and data are now the defining growth drivers for the global cable industry

For the wire and cable sector, the message is clear. The outlook remains strong, but growth is no longer happening in a straightforward market environment. Manufacturers, suppliers and technology partners must respond to opportunity while also navigating tariffs, cost volatility and changing regional trade flows. The demand is there, but success will increasingly depend on agility, investment and the ability to adapt to a more strategically important and politically influenced marketplace.

Chi Lee’s presentation offered IWMA members a valuable and well-balanced snapshot of where the market stands today. The long-term fundamentals for wire and cable remain compelling, but in 2026 the industry is being asked to manage growth in a world where economics, energy policy and geopolitics are more closely intertwined than ever.